The interbank forex market is the top-tier, over-the-counter system where banks and other large financial institutions trade currencies. With daily turnover exceeding $7.5 trillion according to the 2022 Bank for International Settlements (BIS) Triennial Survey, this market functions as the global financial system’s central nervous system. This is where true price discovery happens, setting the exchange rates that affect global trade, investment, and your personal finances. This article explains the mechanisms banks use to exert influence and projects the market’s evolution into 2026 and beyond.

What Is The Interbank Market? The Core of Global Currency Exchange

The interbank market is a decentralized, over-the-counter (OTC) network that connects the world’s largest banks for the purpose of trading currencies. It is not a single physical location but rather a global web of credit relationships that allows top-tier institutions to transact directly with one another. This wholesale market is distinct from the retail market due to its massive transaction sizes, where a standard lot is typically $1 million to $5 million. The interbank market’s primary functions are to facilitate international trade for corporate clients, manage currency risk for institutions, and act as the ultimate source of liquidity and pricing for the entire foreign exchange ecosystem.

The Tier 1 Liquidity Providers: Who Are The Titans of The Interbank Market?

The titans of the interbank market are the Tier 1 liquidity providers, a group of “bulge bracket” banks that handle the majority of global currency trading volume. These banks dominate because of their massive balance sheets, global operational footprints, advanced trading technology, and extensive bilateral credit lines established with one another. The list of top banks by market share evolves, but according to sources like the Euromoney FX Survey, it consistently includes the following institutions:

- JP Morgan

- UBS

- Deutsche Bank

- Citi

- HSBC

- Bank of America

- Goldman Sachs

- BNP Paribas

In recent years, the influence of non-bank liquidity providers, also known as non-bank electronic market makers, has grown. Firms like XTX Markets and Citadel Securities now compete directly with top banks, using sophisticated quantitative strategies and technology to provide tight pricing and deep liquidity, particularly on electronic platforms.

The Mechanics of Interbank Trading: How Trillions Are Exchanged Daily in 2026

In 2026, trillions in currency value are exchanged daily through a highly sophisticated electronic infrastructure that has largely replaced the traditional phone-based dealing rooms of the past. The immense speed, volume, and efficiency of modern forex trading are facilitated by advanced technology. Trading between banks primarily occurs through two main channels: direct bilateral dealing between two parties and trading via specialized electronic brokerage platforms, which aggregate liquidity from multiple participants.

Primary Trading Venues: EBS and Refinitiv Matching

The historic primary electronic trading venues for interbank spot trading are EBS and Refinitiv Matching, which function as central limit order books (CLOBs) where banks can trade anonymously. Although the modern market is more fragmented with liquidity spread across numerous platforms, these two remain critical reference points for global pricing. EBS, owned by CME Group, and Refinitiv Matching, owned by the London Stock Exchange Group (LSEG), have traditionally specialized in different currency pairs. A comparison of these primary venues highlights their distinct roles.

| Feature | EBS (CME Group) | Refinitiv Matching (LSEG) |

|---|---|---|

| Primary Pairs | Dominant in major spot pairs like EUR/USD, USD/JPY, and USD/CHF. | Dominant in Commonwealth pairs (e.g., AUD/USD, NZD/USD) and many emerging market currencies. |

| Function | Anonymous central limit order book for spot FX. | Anonymous central limit order book for spot FX. |

| Market Role | A primary source of price discovery and liquidity for its core currency pairs. | A key venue for price discovery and liquidity, especially in its specialized pairs. |

The Role of CLS: Mitigating Settlement Risk

Continuous Linked Settlement (CLS) is the primary financial market infrastructure (FMI) used to mitigate settlement risk in the interbank market. Settlement risk, also known as “Herstatt risk” after a 1974 German bank failure, is the danger that one party in a foreign exchange trade defaults on its payment after its counterparty has already paid. The CLS system solves this problem using a Payment-versus-Payment (PvP) mechanism. This process ensures that the final transfer of one currency occurs only if the final transfer of the counter-currency also occurs. CLS, operated by CLS Group, is a critical piece of infrastructure that underpins the stability of the entire global currency market by removing the principal risk from trillions of dollars in daily transactions.

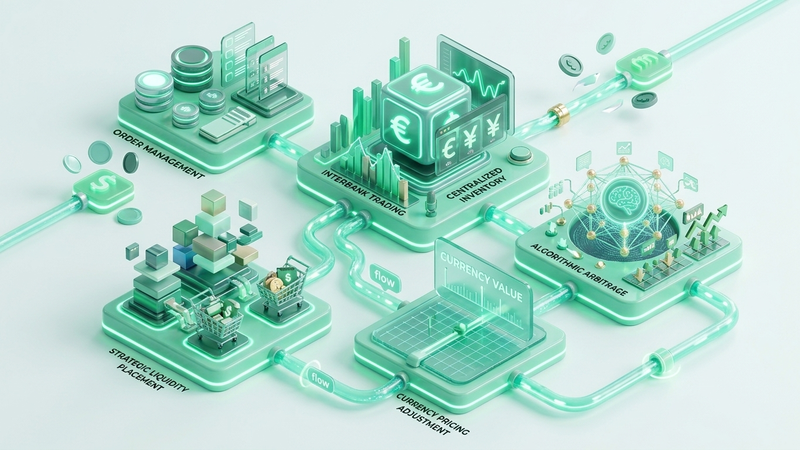

How Banks Actively Move Currency Prices

Banks actively move currency prices through three primary activities: their constant market-making operations, the methodical execution of very large client orders, and strategic positioning based on their unique analysis of market-wide order flow. These activities, conducted both on behalf of clients and for the bank’s own account management, are the main drivers of short-to-medium-term price fluctuations in the forex market. The aggregation of these actions across all major banks creates the observable price movements in currency pairs.

Driving Volume Through Market Making and Spreads

Banks drive trading volume and influence prices through their function as market makers, which involves constantly providing a two-way quote with a bid price (to buy) and an ask price (to sell). The bank profits from the bid-ask spread, which is the small difference between these two prices. The collective quotes from all major banks form the global interbank spread, and the tightness of a bank’s individual spread signals its competitiveness. Market makers use a specific process to manage their inventory and associated risk, which in turn transmits price pressure through the system. This process includes these actions:

- Absorbing smaller client orders directly onto their trading book.

- Adjusting their bid and ask quotes dynamically to attract buying or selling interest, which helps keep their overall position relatively flat.

- Offloading significant, unwanted risk by executing large trades with other banks in the interbank market, an action that directly impacts prices on platforms like EBS and Refinitiv.

Executing Large Client Orders and Managing Risk

The execution of large client orders creates sustained buying or selling pressure that methodically moves currency prices, even when managed with sophisticated tools. These “real money” flows originate from corporations conducting mergers and acquisitions (M&A) or repatriating foreign profits, as well as from large asset managers rebalancing global portfolios. For example, if a U.S. corporation needs to acquire billions of British pounds to purchase a UK-based company, it will approach a Tier 1 bank’s trading desk. The desk cannot purchase this amount at once without causing a massive price spike. Instead, the bank uses execution algorithms like TWAP (Time-Weighted Average Price) or VWAP (Volume-Weighted Average Price) to break the large order into many smaller pieces and execute them over a set period to minimize market impact. How do banks manage large orders and risk? Even with these algorithms, the sustained buying pressure is detectable by other market participants’ algorithms, which causes the price of GBP/USD to grind higher. The bank must also actively hedge the price risk it takes on its own books while working the client’s order.

The Evolving Role of Proprietary Trading Post-Volcker Rule

The Volcker Rule, a key component of the Dodd-Frank Act of 2010, significantly restricted proprietary trading at U.S. banks, altering how they take speculative positions. Proprietary “prop” trading is the practice of a bank trading financial instruments with its own money for direct profit, rather than on behalf of a client. Following the rule’s implementation, banks adapted by either shifting these activities to desks that are permitted to take risk, such as market-making, or by seeing non-U.S. banks and non-bank trading firms fill the void. While large-scale, dedicated prop desks at major banks have been curtailed, banks still leverage the powerful informational advantage gained from seeing massive client order flow. This insight allows them to position their market-making books more profitably, effectively embedding speculative views within their permitted risk-management activities.

The Role of Central Banks and Monetary Policy in The Interbank System

Central banks establish the broad macroeconomic environment through monetary policy, and interbank currency traders’ primary job is to anticipate and position for these policy actions. Commercial banks do not operate in a vacuum; they react to the conditions set by central banks like the U.S. Federal Reserve (via its Federal Open Market Committee or FOMC), the European Central Bank (ECB), and the Bank of Japan (BoJ). Why does monetary policy affect currency values? The main tools central banks use to influence exchange rates are interest rate decisions, as rate differentials are a primary driver of currency value. Other tools include quantitative easing or tightening, which affects money supply, and forward guidance, which signals future policy intentions. A central bank can also perform a direct intervention by buying or selling its own currency in the interbank market, often using a Tier 1 bank as its agent to execute the transactions and influence the currency’s value.

Prime Brokerage: The Gateway for Non-Bank Players

A Prime Brokerage (PB) is a bundled service where a Tier 1 bank provides credit intermediation and market access to other institutional clients, such as hedge funds, smaller banks, and proprietary trading firms. This service is the primary gateway for a vast amount of speculative volume to enter the interbank ecosystem. Instead of establishing separate credit lines with dozens of liquidity providers, a hedge fund can use a single prime brokerage relationship with a bank like JP Morgan or Goldman Sachs. This allows the fund to trade with multiple other banks and ECNs, including Citi, UBS, and EBS, under the prime broker’s name. The prime broker consolidates the client’s positions and handles the clearing and settlement, while the client benefits from access to top-tier pricing and operational efficiency. The bank, in turn, earns fees and gains valuable insight from the additional order flow.

The Dominance of Algorithmic and AI-Driven Trading in 2026

By 2026, the vast majority of interbank trading volume is executed by sophisticated algorithms, with Artificial Intelligence (AI) now playing a standard, non-experimental role in strategy and risk management. This automation has dramatically increased market efficiency and liquidity but has also introduced risks like “flash crashes,” where prices move sharply in seconds. The algorithms used in the interbank market fall into several main categories. The following list defines the primary types of algorithms used in modern currency trading:

- Execution Algorithms: These are designed to execute large client orders with minimal market impact, using strategies like the previously mentioned TWAP and VWAP.

- Market Making Algorithms: These automatically generate and update bid/ask prices, manage inventory risk, and respond to incoming orders in microseconds.

- High-Frequency Trading (HFT) Algorithms: These specialized algorithms exploit tiny price discrepancies between markets (latency arbitrage), identify short-term statistical patterns, or trade instantly on electronic news feeds.

Looking at 2026, the integration of Machine Learning (ML) and AI is mature. According to analysis from firms like PwC and Deloitte on the future of financial markets, banks use AI for predictive analysis of order flow, real-time sentiment analysis of news and social media, and for optimizing complex hedging strategies far faster than a human could.

Regulation and The FX Global Code of Conduct

The decentralized, over-the-counter forex market is governed by a framework of national regulations and a set of globally recognized principles known as the FX Global Code of Conduct. Major regulations like the Dodd-Frank Act in the United States and MiFID II in Europe have increased transparency by mandating the reporting of derivatives trades to central repositories. However, the most influential guide for behavior in the spot FX market is the Code. Developed by central banks and private sector market participants under the guidance of the BIS after the 2013 FX fixing scandal, the Code establishes a common set of principles for good practice. It covers ethics, information sharing, execution practices (including rules around the controversial “last look” practice), and risk management. While adherence is voluntary, there is immense institutional pressure for all major market participants to sign a Statement of Commitment, making it the de facto standard for conduct in the global currency markets.

Navigating The Complexities: Key Questions Answered

The intricate machinery of the interbank market, from its exclusive participants and high-speed platforms to the influence of algorithms and global regulations, often generates common questions. Understanding this complex system is key to grasping how currency values are truly determined. This next section provides clear, direct answers to some of the most frequently asked questions about the structure of the forex market, clarifying key concepts for a better understanding.

Frequently Asked Questions About The Interbank Forex Market

Can Retail Traders Access The Interbank Market Directly?

No. Retail traders cannot access the interbank market directly because it operates on established credit lines between major institutions and involves transaction sizes in the millions of dollars. Instead, retail traders access pricing that is derived from the interbank market. Your retail broker aggregates prices from its liquidity providers (who may be Tier 1 banks or have a prime brokerage relationship) and adds a markup to the spread before presenting it to you on your trading platform.

What Is A Prime Broker in Forex?

A prime broker in forex is a large bank that provides a bundled package of services, including credit and market access, to other institutional clients like hedge funds or smaller banks. This arrangement allows the client to trade with numerous different liquidity providers through a single credit relationship with the prime broker, which simplifies clearing, settlement, and reporting while providing access to the best available market prices.

What Are The Main Tiers of The Forex Market?

The forex market is structured in three main tiers, each with different participants and levels of access. The primary tiers of the forex market are:

- The Interbank Market (Tier 1): This is the core of the market, consisting of the largest banks trading currencies directly with one another and with major non-bank liquidity providers.

- The Institutional Market (Tier 2): This tier includes hedge funds, corporations, asset managers, smaller banks, and ECNs that access the market’s liquidity through prime brokerage relationships with Tier 1 banks.

- The Retail Market (Tier 3): This tier consists of individual traders who access the market through online retail forex brokers, who act as intermediaries.

Interbank Market vs. Retail Forex Market: What Are The Key Differences?

The key differences between the interbank and retail forex markets relate to participants, costs, transaction sizes, access, and regulation. The interbank market is a wholesale market for institutions, while the retail market is for individuals. The following table compares their main attributes.

| Attribute | Interbank Market | Retail Forex Market |

|---|---|---|

| Participants | Major banks and large financial institutions. | Individual traders. |

| Spreads | Extremely tight (fractions of a pip). | Wider, as it includes the broker’s markup. |

| Transaction Size | Millions of dollars per trade. | Micro, mini, or standard lots (from $1,000). |

| Access | Based on established credit lines. | Based on a margin deposit with a broker. |

| Regulation | Principles-based (FX Global Code) and institutional rules. | Direct client protection rules (e.g., FCA, ASIC). |

The Future of The Interbank Market: Trends, Challenges, and Opportunities Beyond 2026

The future of the interbank market beyond 2026 points toward a continued evolution in its power structure, driven by technology and regulation. The market’s trajectory will be defined by the growing influence of non-bank liquidity providers, the ever-deeper integration of AI into trading and analytics, and a relentless focus on data for a competitive edge. However, this evolution comes with a distinct set of challenges and opportunities that will shape global currency trading. The primary challenges facing the market include:

- Market Fragmentation: As liquidity becomes distributed across a greater number of platforms and dark pools, finding a single, verifiable “best price” becomes more complex.

- Cybersecurity Risks: The market’s complete reliance on electronic systems makes it a high-value target for sophisticated cyberattacks, threatening both individual firms and systemic stability.

- Regulatory Burden: The cost and complexity of complying with an array of global regulations, such as MiFID II and various reporting mandates, continue to increase for all participants.

Amid these challenges, significant opportunities are emerging. The exploration of Distributed Ledger Technology (DLT) presents a potential future alternative to the current settlement systems, promising faster and more transparent transactions. Both the Global Foreign Exchange Committee and the Bank for International Settlements are actively researching DLT’s potential. Furthermore, the growth of new FX derivative products and increasing liquidity in emerging market currencies offer new avenues for trading and risk management.